A recent report from AMI Consulting pinpointed that in recent years thin wall packaging has become a space of dynamic structural changes in the rigid plastics market.

Thin wall packaging is a large and relatively stable market in Europe, with the consumption of 3.1 million tons of polymer in 2015, according to the report. The past few years have been particularly productive for the industry and advances in process technology synergistic with polymer science have enabled changes which have facilitated the emergence of new applications.

Concomitant with these changes have been the changes in the supply chain. The industry actively consolidated and the leaders attempted to re-define and re-structure their businesses to maximize technical competence and to create a stronger negotiation platform, pointed out AMI Consulting.

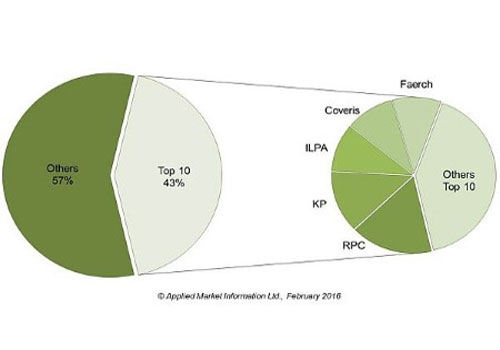

Multi-billion euro converters have started emerging in the global multi-sector packaging arena, including Reynolds (Rank Group), Berry Plastics and Amcor. RPC Group following the acquisition of Promens and Global Closure Systems, and Coveris have reached these ranks as well.

In 2015, the top 10 converters of Thin Wall Packaging in EU28+3 region accounted for 43% of the market. Outside of the leader base, the supply in Europe remains relatively fragmented and more consolidation is expected, according to the report.

Retailers remain ever stronger customers of thin wall packaging, driving improved quality standards of value products. Brand owners employ a range of packaging solutions to capture discrete marketing opportunities, using multiple formats. This enables brand owners to monitor and compare costs, alter the packaging mix and spread risk.

Over the next five years those suppliers with a focused business strategy are expected to continue to strengthen their market position, AMI Consulting analyzed.

Website: www.adsalecprj.com

{kind=link}